.jpg)

Extra Edition! Carbon Market in Focus. Highlights from the Fastmarkets Latin America Carbon Forum 2025.

- Art Dam

- Aug 13, 2025

- 12 min read

Wednesday, 13 August 2025.

The first edition of the Fastmarkets Latin America Carbon Forum was held on August 11, 2025, in São Paulo, Brazil, marking a new chapter in Fastmarkets' operations in the region.

Recognized as one of the leading multi-sector price reporting agencies, Fastmarkets operates in the agriculture, forestry products, metals, and mining markets, providing its clients with strategic information for short- and long-term decisions.

The event preceded the 20th edition of the Fastmarkets Forest Products Latin America Conference 2025 and consolidated Fastmarkets' association with carbon markets, particularly in the context of the event. The initiative was supported by Samaúma, Universidade do Carbono, Acotepac, and Carbon Credit Markets, which served as media partners.

According to Flávio Ojidos of Jataí Capital e Conservação, the forum was characterized by excellent organization and panels featuring renowned experts, who provided consistent analyses and productive discussions, generating valuable insights. Flávio emphasized that the event "excellently" fulfilled its role of fostering a quality debate, contributing to climate literacy and the development of the national market, in addition to highlighting areas of focus for the efficient and transparent implementation of the Brazilian Emissions Trading System (SBCE).

Attorney Rui Fernando Ramos Alves commented: “It was a pleasure to be part of the panel and reflect on what the carbon market will look like in the future, especially regarding the points of attention regarding new securities and the CVM’s actions.”

Check out the main highlights presented in each of the event's panels below.

(1) Workshop: Carbon 101

The Carbon Markets 101 workshop, led by Fastmarkets by Gabriel Reis, Forest Carbon Analytics, and Josh Cowley, Head of Research, offered a clear introduction to carbon markets, highlighting the global climate challenges and the limits of current policies to curb global warming. Even with announced actions, the average temperature already exceeds the 1.5°C target of the Paris Agreement. Concepts such as carbon accounting (Scopes 1, 2, and 3), types of markets (regulated and voluntary), and the fundamentals of offsets, which must be verifiable, additional, permanent, and leak-free, were covered.

The course also explored how carbon credits are created and used globally, the main project types and methodologies—with a focus on comparing REDD+ and ARR—and the role of registries in project pricing and valuation. Current trends include the valorization of high-integrity projects, the advancement of durable removals, and the strengthening of market infrastructure, all of which contribute to making carbon markets more effective and reliable.

(2) Building the Future from Brazil: Where Policy Meets Progress in Late America’s Carbon Market

According to Aloisio Lopes Pereira de Melo, Secretary of the Ministry of Environment and Climate Change, Brazil is taking a leading role in building regulated carbon markets in Latin America, driven by legislative advances and growing coordination among government, the private sector, and financial institutions.

The recent approval of the emissions trading law establishes clear obligations, sectoral limits, and an administrative structure that will initially be linked to the Ministry of Finance, with a future transition to a regulatory agency.

He also commented that the country already has sectors experienced in emissions inventory, and the implementation initially foresees free allowances, followed by auctions. The efforts have received technical support from the World Bank and integration with a financial market. Initiatives such as the Climate Fund and Eco Invest reinforce Brazil’s leadership, while companies with forest assets will be able to account for carbon credits, and insurers are beginning to get involved, despite legal challenges.

On the international stage, Aloisio highlighted the strategic use of mechanisms under the Paris Agreement, focusing on Articles 6.2 and 6.4, leveraging Brazil’s ambitious NDC to generate additional results and develop proprietary methodologies.

The voluntary market is also gaining momentum, with BNDES leading efforts in monitoring and engagement with the financial sector.

He concluded by emphasizing Brazil’s trajectory, which dates back to the Clean Development Mechanism (CDM), and which now consolidates its position as a reference, helping shape the future of carbon in Latin America.

(3) Global Carbon Markets Outlook

Fastmarkets data presented by Carl Peters, Senior Economist show that the global carbon credit market is undergoing a structural transformation, with projected growth of 6.5 times by 2030. Demand is diversifying, with greater prominence of regulatory markets, Article 6 of the Paris Agreement, and CORSIA, which is backed by MIGA (World Bank) insurance.

There is a growing emphasis on project integrity, driven by reports such as those from The Guardian, which have influenced price trends. Methodologies are becoming more conservative, and there is a valuation shift toward high-quality credits, especially durable removal types such as BECCS, DACS, and biochar, whose prices are expected to fall between 2025 and 2030, reflecting greater scale: from US$ 420 to US$ 163 in the case of BECCS, and from US$ 230 to US$ 108 for biochar. Meanwhile, reduction credits, such as REDD+ and ARR, are expected to rise: from US$ 6 to US$ 12 and from US$ 25 to US$ 38, respectively.

South America is consolidating as one of the main emission hubs, with around 20% of global potential by 2030, with 90% of that volume concentrated in REDD+ projects. The pulp and paper industry is expected to contribute significantly to Brazil’s leadership, while retirements are projected to grow globally by 3.4 times between 2025 and 2030.

Demand in the voluntary market tends to stabilize as 2030 approaches, but buyers are becoming more sophisticated, securing volumes through advance contracts. There is a risk of supply shortage, even in the absence of penalties in major emitting economies. Projects that meet quality criteria—verifiability, additionality, and permanence—will receive premium pricing and have greater potential for use, including in regulated systems.

(4) Price vs. Quality: What’s Driving Carbon Credit Value in Latin America?

The presentation by Sam Crew, Strategic Markets Editor – Voluntary Carbon Markets at Fastmarkets, highlighted the key factors influencing the value of carbon credits in Latin America, especially in ARR (Afforestation, Reforestation, and Revegetation) projects. Native species carry a 30% premium over exotic ones, and multi-species projects are valued up to 40% higher than monocultures.

Credits certified under the Gold Standard (GS) can be worth up to 70% more than those from Verra, although this difference is expected to narrow with the adoption of methodology VM0047, focused on ARR projects. Moreover, ARR credits experience less depreciation due to vintage (year of issuance) compared to REDD+.

Project quality, measured by ratings such as those from BeZero, has a strong impact on pricing: ARR credits rated BBB can be worth up to 5.5 times more than those rated C, but are ten times less available. In the case of REDD+, projects rated AA can be worth 4.75 times more than those rated C, although specific factors still cause variations within rating bands.

The trend is for buyers to prioritize higher-rated projects, especially in segments like IFM (Improved Forest Management), where removal credits command significant premiums and enjoy greater market acceptance.

(5) Beyond the Offset: What Makes a Credit Truly High Quality?

During the panel moderated by Sam Carew from Fastmarkets, key issues surrounding the integrity of carbon credits, especially in ARR projects, were discussed.

Cassio Souza from Verra highlighted the four pillars of integrity presented by Gabriel Reis and posed the question: “Is the market willing to pay the price to bring forests back?” He pointed out that changes in Brazilian legislation and certification systems could increase the adoption of ARR credits, provided there is financial willingness. Looking ahead, Cassio foresees greater digitalization, more auditable co-benefits, and advances in project credibility.

Chamss Ould from dClimate reinforced that quality is relative, as it depends on the connection between seller and buyer, and that higher quality comes at a higher cost.

Julio Natalense from SGS emphasized the importance of robust quantification, replicable technologies, avoiding leakage, and developing realistic local standards. When asked how to ensure integrity over 40 years in nature-based solutions (NBS) projects, he pointed to the challenge of land ownership, which requires ongoing responsibility and supporting technology. Additional comments suggested the use of buffer pools and even insurance as protection mechanisms. Julio concluded by highlighting Brazil’s progress in recent years, with methodologies adapted to local conditions.

(6) Attracting Capital: A Forest Carbon Success Story from Brazil

The presentation by Symbiosis Investimentos, delivered by Alan Batista at the Latin America Carbon Forum 2025, highlighted how the company has become a reference in high-integrity forest projects in Brazil. Founded in 2010, Symbiosis works with native species and sustainable management in the Atlantic Forest biome, integrating ecological restoration, premium timber production, and carbon credit generation. With over 2,500 hectares under management and 1.6 million trees planted, it has attracted investments from funds such as Apple’s Restore Fund and Goldman Sachs, thanks to its ability to scale, diversify revenue streams, and meet rigorous environmental and social criteria.

In fact, it’s worth referencing the publication Apple’s Carbon Removal Strategy, which includes compelling charts categorizing a variety of options for removing carbon from the atmosphere using a combination of photosynthesis and chemical processes. These approaches include existing climate solutions such as afforestation and reforestation, as well as relatively new technologies like direct air capture (DAC) and ocean alkalinization.

Alan also noted that to overcome challenges such as high costs, regulatory complexity, and a low conversion rate of eligible projects (only 3%), the company invests in innovation, education, and development of the forest value chain, including nurseries, sawmills, and certifications like FSC and VCS.

At the end, when asked how the company obtained permission from landowners to operate on leased lands and build partnerships for land-use change, Alan explained that Symbiosis works with 10-year lease contracts.

(7) Incorporating Carbon Assets into Timberland Valuations

The panel moderated by Gabriel Reis from Fastmarkets discussed the growing incorporation of carbon assets into forest land valuations, a practice that is beginning to gain traction in Brazil.

According to consultant Jefferson Mendes (BM2C), carbon should be treated as another forest product, alongside biodiversity, integrating into the economic cycle of the forest. Although appraisals that consider carbon value already exist, they remain marginal and face challenges such as inclusion in cash flow and comparison with established biological assets. The business model that enables carbon credits is still under development and, according to him, should not be seen as a speculative race, but rather as part of a new green economy.

Bruno Martins (MOMBAK) highlighted their focus on ARR (Afforestation, Reforestation, and Restoration) in the Amazon, where carbon represents 100% of revenue in some projects. The arrival of this specialized asset is changing the regional dynamic, influencing landowners and competing with sectors such as livestock and the pulp industry. Land valuation now considers carbon as a new opportunity, still in the consolidation phase, but with transformative potential for the forestry sector, as reinforced by Beatriz Lutz (Pátria).

Marcelo Wiecheteck (STCP) emphasized that carbon monetization is becoming increasingly strategic, especially for corporate public image.

(8) Latin America Forest Based Carbon - Market Outlook

The presentation by Gabriel Reis shows that Latin America leads globally in forest credit issuance, with over 280 million units issued — 80% of them through REDD+ projects. Brazil, Peru, and Colombia account for 75% of the regional total, and Latin American credits tend to be more valuable than those from other regions, especially when associated with standards like Gold Standard and high ratings. This valuation is linked to the technical quality of the projects, biological diversity, and growing demand for removal credits.

In Brazil, there are 3.4 million hectares in active projects and expansion potential exceeding 11 million hectares. Forest credit issuance is growing at around 10% per year, with emphasis on ARR and REDD+. National regulation is advancing with requirements for tracking and emission compensation, and the carbon market is beginning to impact sectors such as pulp and paper, by competing for productive land. The country is consolidating as a continuous source of forest credits, with strong influence on pricing and the global dynamics of the sector.

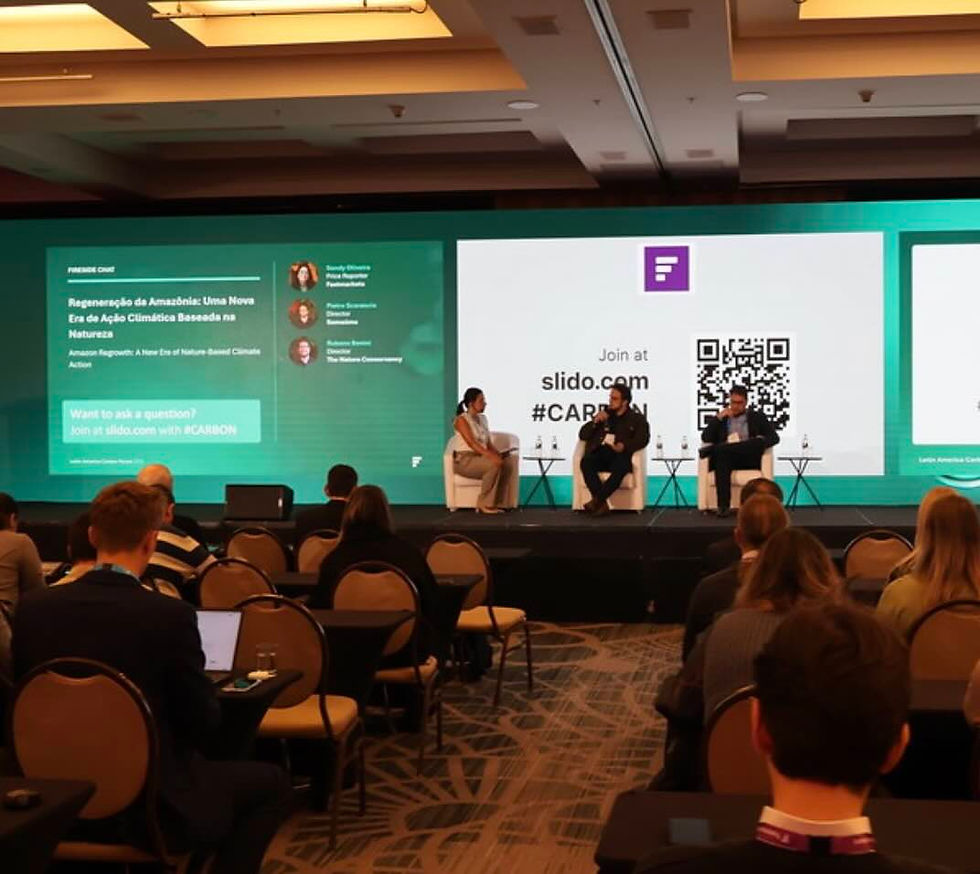

(9) Amazon Regrowth: A New Era of Nature-Based Climate Action

In a panel moderated by Sandy Oliveira (Fastmarkets), experts discussed the challenges and opportunities of nature-based climate action in the Amazon.

Rubens Benini (The Nature Conservancy) commented on criticisms of the avoided deforestation model practiced over the past 2–3 years, pointing out structural limitations. He also highlighted the arrival of private capital into the carbon market, but warned of regulatory hurdles, lack of financing, and the need for stronger governance mechanisms to ensure project integrity.

Pietro Scarascia (Samaúma) emphasized that a restoration project must be economically viable, with the credits generated covering operational costs — and that team qualification is a decisive factor. He advocated for a strict-sense restoration approach in the deep Amazon, which requires an additional economic nexus, different from the reality of, for example, the Atlantic Forest. Among the main challenges, Pietro cited acculturation, the tropicalization of processes, including the legal aspect, as a barrier to scalability and project effectiveness.

(10) Carbon Policy in Motion: Brazil’s Role in Shaping Latin America’s Carbon Future

In the panel moderated by Pedro Venzon (IETA), experts discussed the legal and institutional challenges for the operation of the regulated carbon market in Brazil.

Renata Campetti Amaral (Trench Rossi Watanabe) emphasized that the government structure equipped to run the system is expected by the end of the month, but there are still uncertainties regarding interaction with international trade and which credits will be accepted. She identified land tenure issues as one of the main obstacles and compared carbon credit projects to environmental licensing, saying both carry the burden of trying to solve all the country’s problems. She also stressed the importance of clear methodologies to ensure the system’s integrity.

Ludovino Lopes warned that the market structure is still incomplete, lacking a “house map” to guide topics such as corresponding adjustments and ITMOs, especially given the high ambition of Brazil’s NDC. He likened the situation to several rooms being built simultaneously without a defined blueprint, and reinforced that time is short and intertwined with the political agenda. Once the regulated market begins operating, it will influence prices, governance, and other markets. Ludovino illustrated the journey of a carbon credit, which may start as a voluntary credit worth US$ 2–3, and if well structured, reach US$ 45–50 in the international regulated market.

Rui Alves, meanwhile, brought the client’s legal perspective, highlighting the role of CVM and the need for a structured relationship with the market, including regular reports, material facts, and a long-term vision—similar to assets with a horizon of decades.

(11) From Ambition to Action - What are Carbon Credit Buyers Looking for?

In the panel moderated by Eduardo Ferreira (The World Bank), participants discussed the expectations of carbon credit buyers, with a focus on integrity, transparency, and innovation.

Miguel Chavarría (South Pole) highlighted the role of Article 6 and CORSIA, noting that the Mexican market remained on paper for five years, hindered by insufficient capacity building. He emphasized the current wave of innovation, with projects in offshore wind, green hydrogen, batteries, and floating solar, as well as South Pole’s own evolution—now conducting more rigorous risk assessments and supported by a robust team.

Leonel Mello (Volkswagen Climate Partner) and Lázaro Gouveia Matheus (Auren Energia) reinforced the current focus on the voluntary market, with growing attention to standards, ratings, and social due diligence. Leonel pointed out that Volkswagen, previously focused on REDD+, now invests in hydrogen, CCS, and biochar, with strict field protocols and engagement with local communities. Lázaro mentioned an international due diligence process that lasted 10 months, validating social co-benefits.

Tomas Garcia (Itaú BBA), meanwhile, noted that the bank is still a small buyer, without formal mandates, in a wait-and-see phase regarding the government and Article 6. He stressed the need for clear methodologies, pricing mechanisms, and legal certainty, citing the ALM project with Citrosuco as an example of corporate innovation.

🏆 If you have an interesting story about carbon credits in your country, our audience already reaches over 100 nations! Send your message directly through our LinkedIn page.

Sign up at www.carboncreditmarkets.com to receive insights, news and media updates.